Financing a new home build is fundamentally different from buying an existing home—but it doesn't have to be intimidating. For Gulf Coast buyers in Florida and Alabama, understanding construction loans is the key to turning your dream home from blueprint to reality without financial stress.

At Delta Max General Contractor, we guide hundreds of families through the construction financing process every year. This guide breaks down construction-to-permanent loans, draw schedules, and qualification requirements specific to building in hurricane-prone coastal zones.

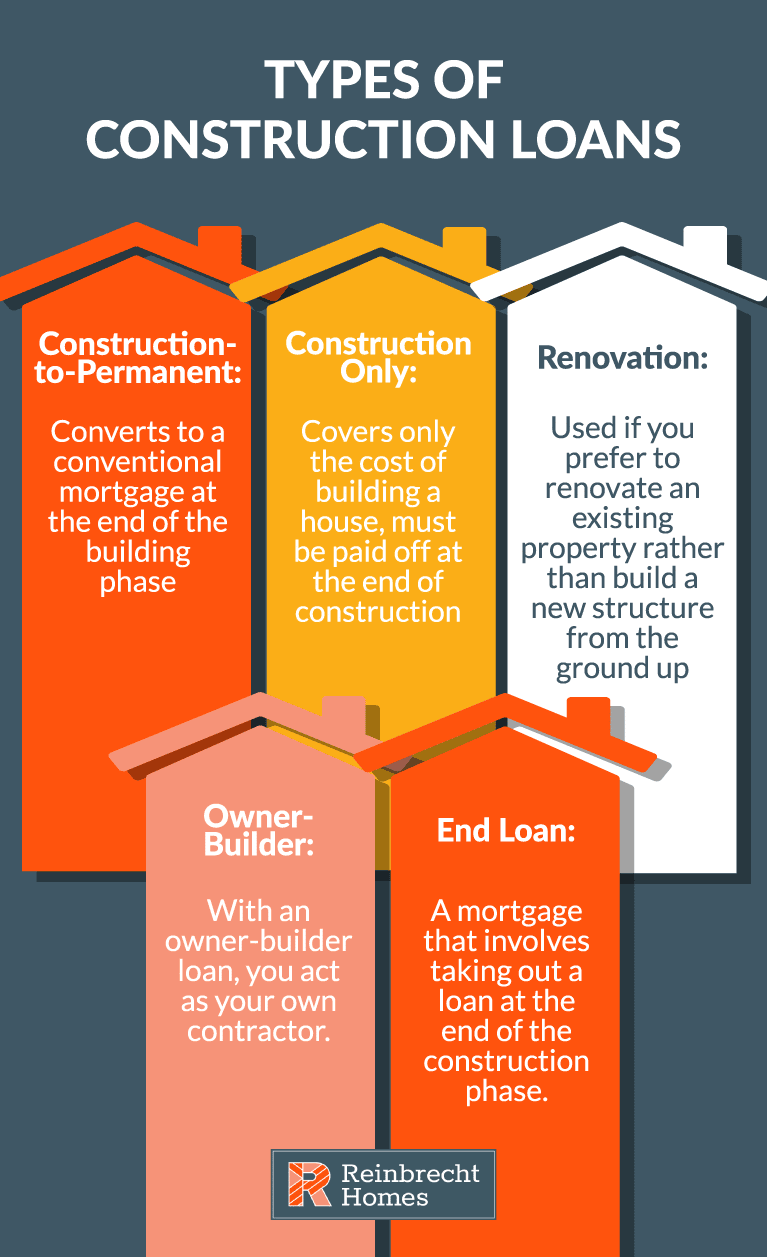

What Is a Construction-to-Permanent Loan?

Unlike a traditional mortgage that funds a completed home purchase, a construction-to-permanent loan (also called a "single-close" or "one-time close" loan) finances the building process and then converts to a standard mortgage once construction is complete.

How Construction Loans Work: The Basics

- Construction Phase: You pay interest-only payments on funds as they're disbursed to the builder

- Draw Schedule: Money is released in stages (draws) as construction milestones are completed

- Conversion: Once the home is complete, the loan automatically becomes a traditional mortgage

- Single Closing: You pay closing costs once, not twice (saving $3,000-$5,000 compared to two-close loans)

The Draw Schedule: Funding Your Build Step by Step

Construction loans use a "draw schedule" to release funds as your home progresses. This protects both you and the lender by ensuring money is available when needed while verifying work is completed satisfactorily.

A typical Gulf Coast custom home draw schedule looks like this:

- Draw 1 (Lot Acquisition/Prep): 10-15% — Covers land purchase (if included) or lot prep, clearing, and initial permits

- Draw 2 (Foundation): 15-20% — Slab or piling foundation completion, especially critical in flood zones

- Draw 3 (Framing): 20-25% — Rough framing, roof structure, and weatherproofing

- Draw 4 (Mechanicals): 15-20% — HVAC, electrical, plumbing rough-in, and hurricane strapping

- Draw 5 (Drywall/Interior): 15-20% — Insulation, drywall, trim, and interior finishes

- Draw 6 (Final/Completion): 10-15% — Flooring, paint, fixtures, final inspections, and certificate of occupancy

Each draw requires an inspection to verify work is complete before funds are released. At Delta Max GC, we coordinate these inspections seamlessly to prevent delays.

Qualification Requirements: What Lenders Look For

Credit and Income Standards

Construction loans typically require stricter qualifications than traditional mortgages:

- Credit Score: 680+ preferred (some lenders accept 640+ with compensating factors)

- Debt-to-Income Ratio: Maximum 45% (including your current housing payment and the new construction loan)

- Income Documentation: 2 years of tax returns, W-2s, and recent pay stubs; self-employed borrowers need additional documentation

- Reserves: Most lenders require 6-12 months of mortgage payments in savings after down payment

Down Payment Expectations

Construction loans typically require larger down payments than conventional mortgages:

- Standard: 10-20% of total project cost (land + construction)

- Jumbo Loans: Often 20-25% for loans exceeding conforming limits ($766,550 in most Gulf Coast counties in 2024)

- Land Equity: If you already own your lot, its appraised value can count toward your down payment

Interest Rates During Construction

During the building phase, you'll pay interest-only on the amount drawn (not the full loan amount). This keeps payments manageable while your home takes shape.

Rate Considerations:

- Construction loan rates are typically 0.5-1% higher than permanent mortgage rates during the build phase

- With a single-close loan, your permanent rate is often locked at closing, protecting you from rate increases during the 4-6 month build

- Interest payments during construction are often rolled into the loan (called "interest reserve"), meaning you pay nothing out-of-pocket until move-in

Gulf Coast Special Considerations

Hurricane and Flood Insurance Requirements

Building on the Gulf Coast means lenders will require specific insurance coverage before releasing funds:

- Builder's Risk Insurance: Required from day one, covering materials and partially completed structure against storm damage

- Flood Insurance: Mandatory for properties in FEMA flood zones (most beachfront and many inland Gulf Coast properties)

- Wind/Hurricane Coverage: Florida and Alabama lenders require specific windstorm policies, often with higher deductibles for named storms

These insurance costs are typically escrowed and included in your final mortgage payment. We recommend budgeting $3,000-$6,000 annually for comprehensive coverage on a $400,000 Gulf Coast home.

Appraisal Challenges in New Developments

If you're building in a new area without many comparable sales, lenders may require:

- Additional comparable properties from wider geographic areas

- Documentation of pre-sales in the community

- Higher reserves or larger down payments to offset perceived risk

Building in established areas like Pensacola or Gulf Shores typically presents fewer appraisal challenges than remote waterfront locations.

VA and FHA Construction Loans

VA Construction Loans for Veterans

Qualified veterans can build with $0 down using VA construction loans:

- No down payment required (though some lenders may require 5% for construction phase)

- No private mortgage insurance (PMI)

- Competitive interest rates

- Limited to primary residences only

Not all lenders offer VA construction loans, but several national banks and credit unions serve Florida and Alabama veterans. We work with VA-approved lenders familiar with Gulf Coast building requirements.

FHA Construction Loans (203k Alternative)

FHA construction loans allow down payments as low as 3.5%:

- More lenient credit requirements (580+ credit score)

- Higher debt-to-income ratios allowed (up to 50%)

- Mortgage insurance premium (MIP) required for life of loan

- Loan limits apply ($498,257 for most Gulf Coast counties in 2024)

Ready to Explore Financing Options?

Don't let financing questions delay your dream home. Browse our available floor plans with transparent pricing, then connect with our preferred lenders who specialize in Gulf Coast construction loans.

Browse Home Plans & PricingCommon Construction Loan Mistakes to Avoid

1. Underestimating Total Project Costs

Include not just construction, but land costs, permits, impact fees (which can run $5,000-$15,000 in Florida), utility connections, and landscaping. Lenders require a 5-10% contingency reserve for overages.

2. Changing Plans Mid-Construction

"Change orders" can delay draws and increase costs. Finalize your design before breaking ground to avoid financing complications.

3. Not Locking Your Permanent Rate

If you choose a two-close loan or don't lock your rate, rising interest rates during construction could significantly increase your monthly payment.

4. Working with Inexperienced Lenders

Construction loans require specialized knowledge. Work with lenders who regularly finance Gulf Coast builds, not just standard mortgages.

FAQ: Construction Loan Questions

Can I use the equity in my land as a down payment?

Yes. If you own your lot free and clear, most lenders will accept its appraised value as your down payment contribution, potentially allowing 100% financing of construction costs.

What happens if construction goes over budget?

You'll need to pay overages out-of-pocket or obtain a loan modification. This is why we emphasize detailed upfront budgeting and maintaining contingency reserves.

Can I act as my own general contractor?

Most lenders require a licensed general contractor (like Delta Max GC) to oversee construction. Owner-builder loans exist but require significant experience and larger down payments (typically 25%+).

How long do I have to complete construction?

Most construction loans allow 6-12 months for completion. Extensions are possible but may incur fees. Our typical build timeline is 4-6 months, well within standard limits.

Do I make payments during construction?

With most single-close loans, interest is capitalized (added to the loan) during construction, meaning you pay nothing until move-in. Verify this with your lender.